Looking at Our Portfolio

As we head into the fall season, the equity market has improved significantly from its bleak lows in March. However, even though we are beating the S&P 500 (an index of large caps stocks) our portfolio has not fully recovered. Year-to-date, we are up 17.4% compared to 15.1% for the S&P500.

There are several tools, some of which were developed by NAIC / BetterInvesting for looking at an entire portfolio. The portfolio evaluation review technique or “PERT” takes data from individual stock selection guides and creates a table. Sorting this information allows identification of the outliers.

PERT Report. Here is the PERT Report for the Mose Pond Investors portfolio. This report is sorted on estimated total return, lowest to highest. Looking at the low end, several companies in our portfolio stand out as being candidates for replacement, e.g., AIG, Helmerich & Payne (HP), and Illinois Tools Works (ITW).

Before making any decisions based on the PERT report, it is important to understand how Toolkit 6 calculates total % return. The PERT report uses the estimated earnings per share (EPS) for the next 12 months and extends those earnings for four more years (for a total of five years) using the EPS growth rate from section 1 of the SSG. The 5-year estimated EPS is multiplied by the estimated future PE (which is the average of the high and low PE from section 4 of the stock selection guide). This give an expended price in five years. 5-year price appreciation then is a simple calculation — [(Future Price / Present Price) ^ (1/5)] – 1.

The total return is the the sum of the price appreciation in percent and the average dividend payout in percent. This may sound complicated, but it is not. The total return calculation depends on the accuracy of the 12 month projected EPS, the applied 5-year EPS growth rate and the estimated future PE. Despite the wonderful precision of the software, PAR is just a reasoned guess based on three independent variables.

The return on any stock is a function of only three variables: earnings, dividends, and valuation (i.e., the price to earnings ratio). When we try to predict earnings or PE ratios five years into the future, we must use judgment and we are often wrong. That is why we revisit our judgment each quarter as companies publish new earnings reports.

Trend Report. This Trend Report looks at the trend of the operations of the companies in the portfolio over two consecutive quarters relative to earnings, sales, and pre-tax profit in order to view the “trend of the trends.” The report also includes total return (as described above) and projected average return or PAR.

Projected average return or PAR is calculated in a manner similar to similar to total return except that we use Section 1 of the stock section guide rather than the analysts 12-month estimates for future EPS. There are several different techniques for estimating future EPS, but projected average return or PAR is based largely on the 5-year estimated EPS in Section 1 of the SSG. The total return and PAR sometimes differ. This simple reflects the different approaches to calculating 5-year EPS.

Portfolio Allocation. It is important to understand how what asset classes are included in a portfolio. For U.S. equities, we generally characterize a stock as small, medium, or large based either ion market capitalization or total revenue. We also use fundamental analysis to characterize a stock a growth, value, or in between. In a globalized economy, it is helpful to know the extent to which a company’s revenue come from outside the U.S.

Academic studies have show that small cap stocks out perform large cap stocks over time. Similarly, value stocks tend to slightly out perform growth stocks over long periods. Also diversifying a portfolio over multiple asset classes tends to reduce risk and improve ove7rall performance.

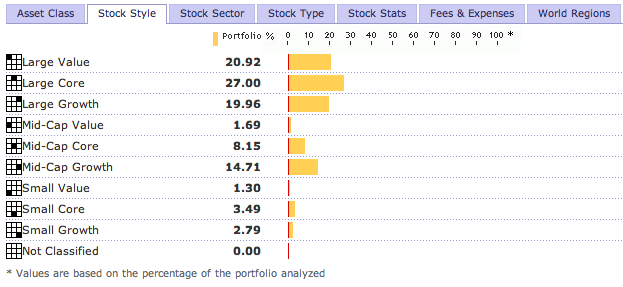

Morningstar provides an excellent “X-Ray” tool for looking at the style and sector characteristics of a portfolio. Here are the X-Ray summaries for the Mose Pond Investors portfolio by style and sector. These reports suggest that the portfolio may be overweighted to large cap stocks.

{kind=link}

{kind=link}

As if all these views of our portfolio were no confusing enough, there is one more. The Manifest Investing portfolio dashboard is helpful. It shows quality and PAR for the portfolio. For the reasons discussed above, our calculation of PAR may not agree with those on Manifest Investing. However, the portfolio dashboard does provide an easy way to find outliers which require more analysis. The portfolio dashboard also provides any easy why to decide where to apply additional case (i.e., those companies with high quality and high PAR that reflect a small percentage of the overall portfolio. Conversely, the portfolio dashboard can be used to find stocks to replace (i.e., those with low PAR or quality that reflect a large percentage of the portfolio.

Taking a Long Term View

Warren Buffet’s annual letter to Berkshire Hathaway shareholders should be mandatory reading for all investors. He not only provides an economic outlook, he explains how Berkshire Hathaway makes money for its shareholders. No other publicly traded company provides the same candor or clear explanation of its operations. (All of the Berkshire Hathaway shareholder letters from 1977 to 2008 can be found here.)

Warren Buffet’s annual letter to Berkshire Hathaway shareholders should be mandatory reading for all investors. He not only provides an economic outlook, he explains how Berkshire Hathaway makes money for its shareholders. No other publicly traded company provides the same candor or clear explanation of its operations. (All of the Berkshire Hathaway shareholder letters from 1977 to 2008 can be found here.)

Between 1965-2008, the book value of Berkshire Hathaway shares grew at compounded annual gain of 20.3%. In comparison, the S&P 500 (including dividends) had a compounded annual gain of 8.9%.

Replacing our low PAR Stocks

Using data from our portfolio dashboard on Manifest Infesting, here are some proposed changes to the portfolio.

First, sort the portfolio by projected average return (PAR) to show which stocks have the highest and lowest PAR. You do this by clicking on the PAR column heading or look at this PDF file. (Place your mouse over the embedded yellow note in the PDF file.)

The six stocks on the bottom (highlighted in yellow in the PDF file) have the lowest projected average return. Looking at these stocks, that is not surprising. Two are bank stocks (WFC and SNV). The current housing market adversely impacts LOW. Similarly, a decrease in consumer spending impacts BBBY and WMT.

We should consider replacing all of these except JNJ. (JNJ is a high quality blue chip stock despite the mediocre PAR. It is a keeper.)

Now we can add to our positions in stocks we already own with stocks that have a higher projected average return than those we are replacing.

Look at again at our portfolio dashboard. Now sort by the value this time, so our largest positions are on top and our smallest positions are on the bottom. Look for stocks for which we don’t yet have a 5% position and which have a projected average return of more than 20%. We can would increase our position in those shares to about 5% or $2,000 total.

This PDF file shows the idea. The candidates for replacement are shown with struck through text. These are the five stocks with the lowest projected average return or PAR. The candidates for additional shares are highlighted in yellow.

There are several additional stocks we may want to consider, including ADBE, AAPL, PCP, and PTR. More to follow on this.

How are we doing?

Like the fighter who says “if you think I look bad, you should see the other guy,” a few hard blows have landed on the Moose Pond portfolio but we are still ahead of the broad market indices this year by slightly more than 10%.

Using the performance benchmark report in Bivio, the internal rate of return for the Moose Pond portfolio was a negative 27.6% year-to-date on October 31. In comparison, the Vanguard Total Market Index Fund was down 38.6% and the Vanguard S&P 500 index Fund was down 38.5% for the same 10-month period.

It will take a strong post-election rally to take the edge off the losses for this year. Stock valuations are at a low for several decades. So while there has to be pony in here somewhere, no one can be sure exactly when we’ll find it. In the interim, we should continue to follow out investment objectives and remain fully invested and commit new cash.

We do have an opportunity to replace several of our stocks with ones that have a higher projected average for the next five years. More to follow on that.

Here are performance reports for the one month and 12 month periods ending on October 31, 2008.

Weathering the Storm

Despite the tumultuous week on Wall Street, our portfolio weathered the storm. Since the beginning of the of the year, the value of a unit share in Moose Pond Investors declined about 2% from $13.647 to $13.375. However, the overall stock market declined 13.1% for the same period (using the Wilshire 5000 index). Our internal rate of return, which takes into account all cash flows for the portfolio, for the same period is -2.5%. Here is a detailed YTD performance report.

AIG was the big loser, dropping 93%. The stock is probably a lost cause. Good thing we didn’t but any more! The other contributors to our losses this year were Synovus Financial (-50.8%), Total System Services (-35.2%), Microsoft -28.5%), and Intel (-26.5%).

An astute reader of this blog pointed out that most of the drop in price for Synovus Financial (-50.8%) this year was a result of the spin-off of TSS in January. That’s exactly correct. Just looking at the price of SNV does not tell the whole story.  At the beginning of the year, our holdings in SNV had a value of $1,758. SNV and TSS currently have a combined value of $1,392. So the actual decline in value this year is only 20.8%.

But for the losses on AIG and TSS, we would have been in positive territory for 2008.

We do have some winners this year. They include Helmerich & Payne (+40.3). Wells Fargo & Co. (+36.2%), Amgen (+29.1%), Sun Hydraulics (+26.4%), and Lowes (+26.3%). This underscores the importance of diversification and quality in a portfolio.

Take a look at the portfolio dashboard from Manifest Investing. We may want to consider selling Bed, Bath & Beyond and Brown & Brown. At the same time, we may want to slightly increase our holdings in Microsoft, Walgreen, Transoceanic, and FactSet Research. Each of these companies have a high quality rating and high projected average return.

Market Reaction to Earnings Estimates – SNHY

It is always interesting to watch the market reaction to quarterly earnings reports. Small variances between reported earnings and analyst expectations, especially in growth stocks, frequently result in sharp price fluctuations. More often than not, the change in price has nothing to do with the underlying business model of the company. A case in point is Sun Hydraulics, one of our holdings.

Sun Hydraulics Corp., SNHY, reported Q2 (June) earnings of $0.54 per share, $0.04 better than the First Call consensus of $0.50. Quarterly revenues rose 18.8% year over year to $51.6M vs. the $51.4M analyst consensus. (Q3 earnings press release.)

However, the company reduced its outlook for Q3, projecting EPS of $0.35-0.37 which is slightly lower than the $0.42 analyst consensus. The company also projected Q3 revenues of $45M which is slightly lower than $47.93M analysis consensus. Here is the company’s statement regarding Q3.

“Sun’s products are used in diversified equipment markets around the globe,” stated Carlson. “Many of these markets, such as mining and energy, remain strong and demand is high. In other more obvious markets, such as equipment used in residential and commercial construction, we have begun to see some softening.”

“The diversity of our end markets, both geographically and the segments we participate in, is pivotal to maintaining our growth,” concluded Carlson.

2008 third quarter sales are estimated to be approximately $45 million, a 9% increase over last year. Third quarter earnings per share are estimated to be between $0.35 and $0.37 per share, compared to $0.32 per share last year. EPS estimates for the third quarter include a charge of $775K for U.S. income taxes due on the repatriation of $6 million from Sun Germany in July 2008.

This slightly reduced guidance caused the stock to drop 11.24% on August 5 after it announced its earnings.

Here is an updated stock selection guide that incorporates the Q3 data. It use a conservative estimated of 18% for revenue and sales growth. It also uses a conservative 5-year average average P/E of 16.9. The SSG still shows a projected average return of 13.7%. The fundamental business model of the company has not changed. It is still a strong hold. Despite teh drop in price yesterday, we have a 17.2% annualized return on SNHY.