Annual Report for 2006

In 2006 we had a total return of 6.1%. The value of a unit increased from $13.097 to $13.894. While our return was positive, it lagged behind most of the major market indices. For the first time, we are slightly behind the S&P 500 for a five year period (5.9% vs. 6.2%). Portfolio turnover was about 10%. You can find the annual report for Moose Pond Investors here.

More information about the performance of individual stocks in 2006 can be found in the diversification report and performance report.

How Are We Doing?

So how are we doing so far this year on return? The answer is OK, but not as well as we should be doing. We have an internal rate of return of 7.3% year to date. (Internal rate of return takes into account when we receive funds. It is a more accurate measure of performance.) 7.3% is in line with the Wilshire Large Growth Stock index which is up 8.5%. However, some of the broader market indices have done much better, such as the the Wilshire 5000 which reflects the total market, is up 13.2% for the year.

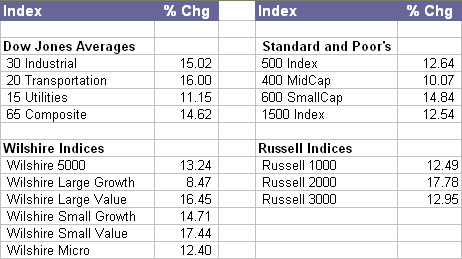

How we are doing depends on the index to which we compare our portfolio performance. Here is a table showing year to date return data taken from the Wall Street Journal as of Wednesday, November 22.

Note that value stocks and small stocks have out performed both large and growth stocks. This has been a trend for a number of recent years. If you want to compare investment returns by asset class (large, small, value growth, etc.) take a look at the Callan Periodic Table of Investment Returns.

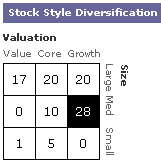

As you can see from the matrix on the right, our portfolio is weighted heavily toward large growth stocks. It was only some recent purchases of GYI and VTI that improved our style balance. Large growth stocks have not done as well as the smaller stocks and the value stocks this year. We need to include more small and medium size companies in our portfolio. It may be inconsistent with an NAIC approach, but we also need some value stocks. Value stocks are generally defined as ones have lower price to earnings or low price to book ratios.

As you can see from the matrix on the right, our portfolio is weighted heavily toward large growth stocks. It was only some recent purchases of GYI and VTI that improved our style balance. Large growth stocks have not done as well as the smaller stocks and the value stocks this year. We need to include more small and medium size companies in our portfolio. It may be inconsistent with an NAIC approach, but we also need some value stocks. Value stocks are generally defined as ones have lower price to earnings or low price to book ratios.

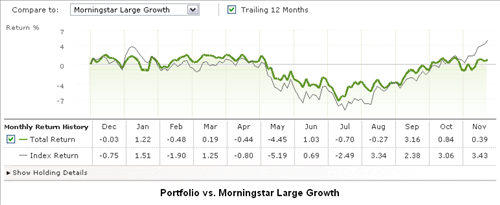

The next two graphs compare our portfolio return over the past 12 months with two Morningstar indices. The first graph compares our return to the Morningstar large growth index. Our return tracks that index fairly closely.

The second graph, below, compares our return with the Morningstar U.S. market index. This is a broad index that includes all stocks. We are not doing as well as that index.

Getting Ready for Winter

Most of our companies have announced their 3rd quarter results. Here is an updated PERT chart (portfolio evaluation review technique). Also, here is the portfolio summary. The average quality rating for the portfolio is 67.5 (65 is very good) and average projected average return is 13.3%.

In looking across the portfolio, two, possibly three, companies seem like good candidates for replacement. These are Marsh & McClennan (MMC) and Affiliated Computer Systems (ACS). The third possibility is Pfizer (PFE). We may want to consider replacing these companies with smaller quality companies with better growth prospects. Also, we should look at adding to our position in some of our better holdings.

Marsh & McClennan has not yet recovered from its myriad of regulatory problems. Click here for a SSG. It has failed to re-establish growth in either revenues or earnings. Return on equity and pretax margins have dipped significantly, with no immediate sign of recovery. It may be a good value stock (Morningstar rates it 4-stars) but it currently fails as a quality growth stock. MMC is a prime candidate for replacement.

Affiliated Computer Systems seems unable to move forward. Click here for a SSG. As the chart below shows, it seem it has been unable to grow its revenue and earnings in any significant way over the past 4-5 quarters. It is now mired in an options pricing mess and will have to restate its earnings. ACS failed to fully report its current quarter and instead offered up instead “non-GAAP” (GAAP = generally accepted accounting principles) metrics of performance. Its TTM pre-tax margin (10.5%) is below the industry average (15.8%). Morningstar still rates ACS 4-stars but also rates it F for stewardship. ACS may be a decent company about to turn the corner — assuming its options pricing problem doesn’t get worse — but it seems to be another prime candidate for replacement.

Pfizer is no longer a classic growth stock. It’s price has rebounded in the last 12 months up more then 22%. However, both growth and quality of earnings are in doubt gonig forward. Sales projections over the next 5 years vary from 2.6% to 6%. Click here for a SSG. PFE might be a good candidate for replacement.

Quarterly Report

We finally saw decent portfolio gains this quarter in the Moose Pond portfolio. Here are the details.

For the quarter justed ended, our net gain is +3.5%. For comparison, the S&P 500 rose +5.2% for the same period. The five stocks advancing the most were: PFE (+21.9%), SYK (+17.8%), UTSI (+13.9%), AMGN (+15.4%), and JKHY (+11.1%). The five stocks declining the most this quater were: MXIM (-6.0%), COF (-7.9%), LOW (-7.3%), OXY (-5.99), and ITW (5.11).

Looking back over the past 12 months, the portfolio gained +6.3%. (compared to 8.7% for the S&P 500). The big gainers were: FDS (+38.6%), IFIN (+31.2%), OXY (+29.4%), BRO (+23.9%), and CBH (+21.3). The decliners were: MXIM (-33.2%), INTC (-11.4%), PDCO (-14.7%), LOW (-14.2%), and COF (-7.9%).

Overall, we have achieved decent performance this quarter. It would be nice to start beating the S&P 500 once again. We need to do a little fine tuning of the portfolio.

YTD Returns

Following up on the earlier posting, this performance report shows year-to-date return for each stock in the portfolio. Stocks with more than 10% return (up or down) are highlighted in yellow. A number of our high quality stocks, have not done well this year.

Stocks down more than 10% year-to-date: COF (-22.9%), LOW (-20.5%), INTC (-16.7%), MMC (-16.1%), AMGN (-13.7%), ACS (-13.2%), and PDCO (-13.0%), Stocks up more than 10% year-to-date: OXY (29.1%), IFIN (+26.0%), PFE (+20.5%), CVX (+15.4%), and SNV (+12.8%). Note that the YTD return is simply a snapshot in time. It does not reflect the overall, long term return we have achieved for these stocks.

We need to to be patient. The business models seem intact for each of the stocks that have declined. (Although we do need to take a hard look at MMC.)

Report for July 2006

In July, the Moose Pond Investors portfolio declined 0.13% while the S&P 500 increased 0.52%. Year to date, the portfolio declined 0.12% while the S&P increased 2.28%. The unit value of a share was $13.12 on July 31.

The biggest gainers in July were Pfizer (PFE) +10.8%, Stryker Corp. (SYK) +8.1%, and Brown & Co. (BRO) +7.4%. The biggest losers were Capital One Financial (COF) -9.5%, Maxim Integrated products (MXIM) -8.5%, and Factset Research (FDS) -7.2%.

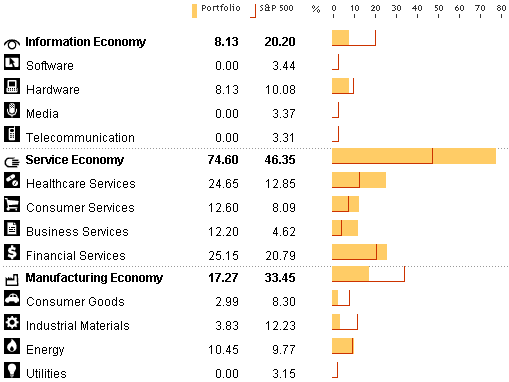

The portfolio remains diversified with 25 holdings. The following chart from Morningstar compares the sector diversification of the portfolio with the S&P 500. In adding to the portfolio, we should probably avoid further overweighting of the services sector.

As the chart on the rights shows, the portfolio consists of large cap (57%), medium cap (38%), and small cap (65%) stocks. We should focus on finding more medium and small cap stocks.

As the chart on the rights shows, the portfolio consists of large cap (57%), medium cap (38%), and small cap (65%) stocks. We should focus on finding more medium and small cap stocks.

Looking at style, the portfolio consist of value (18%), blend (35%), and growth (48%). This mix is probably OK but growth stocks have taking quite a drubbing over the past 12 months. (For a comparison of growth and value stock returns by year see the Callan Periodic Table.)

SSGs Updated

The stock selection guides (SSGs) for each of the stocks in the portfolio have been updated as of June 30. Follow the links in the portfolio summary for the current SSGs.

The PERT Chart and Trend Report also have been updated. The PERT chart is sorted by total return while the trend report is sorted by projected average return.

Mid-Year Report

Unit share price on June 30 was $13.14 up only slightly from the $13.09 at the beginning of the year. The IRR was 0.7%. In comparison, the S&P 500 was up 1.76% for the same six month period. (Actual gain for the S&P will be slightly higher with dividends.)

Top five advancers for the first half of 2006 were: Occidental Petroleum, OXY (+29.4%), Investors Financial, IFIN (+20.2%), FactSet Research Systems, FDS (+15.2%), Chevron, CVX (11.1%), and Maxim Integrated products, MXIM (+5.0%). The five biggest decliners for the same period were: INTC (-20.2%), Amgen, AMGN (-17.6), Affiliated Computer Systems, ACS (-13.8), Marsh & McLennan Companies, MMC (-14.4), and Stryker, SYK (-8.0%).

With the possible exception of MMC, the fundamentals of the decliners remain intact and don’t warrant sale of these stocks. The wide range reflected by the return of the top and bottom stocks for 2006 underscores the importance of diversification and adding regularly to the portfolio.

Quarterly Report

The net asset value for Moose Pond Investors increased +4.1% in the first quarter of 2006. Unit price is up from $13.10 to $13.65. All of the major indices are up as well: the Dow +3.7%, the Nasdaq +6.1%, the S&P 500 +3.7%, and the Russell 2000 +13.7%. See quarterly performance report.

The portfolio summary on this web site has been updated through March 31. (You can find the portfolio snapshot the “Portfolio Summary” section in left side column.) Also, the stock selection guides linked to the portfolio summary has been updated so you can see how we computed projected average return.

Winner and Losers. Winners for the quarter were: Jack Henry & Associates (JKHY) +27.2%, Johnson & Johnson (JNJ) +20.1%, and Occidental Petroleum (OXY) +16.5%. Losers were: UTStarcom (UTSI) -22.0%, Intel (INTC) -21.7, and Amgen (AMGN) -7.8%. Fortunately the winners outflanked the losers and the net gain for the quarter was $1,260.

Transactions. During the quarter, we purchased new positions in Illinois Tool Works (ITW) and Stryker (SYK). We also added to our position on Intel (INTC). We have continued to reinvest dividends as we receive them.

Diversification. Our holdings are spread across six sectors. The financial services sector (27%) remains our largest sector holding, with technology (21.9%) and healthcare (20.9%) the next largest. See diversification report.

Diversification. Our holdings are spread across six sectors. The financial services sector (27%) remains our largest sector holding, with technology (21.9%) and healthcare (20.9%) the next largest. See diversification report.

The Way Ahead. We currently have 26 companies in our portfolio. We only need 17 or so to achieve diversification of nonsystematic risk. Nonsystematic risk results from the volatility of the prices of individual companies. Systematic risk comes from volatility of the overall market (e.g., movement of the market — all or most stocks — as a whole). We can’t diversify for that risk within the portfolio. Some people address systemic risk through asset allocation, i.e., investing in various asset classes. Quality growth stocks might be one such class. This gives us the flexibility to reduce the number of companies, without harming our overall diversification.

Looking at the projected average return (PAR) and the current P/E ratios for the companies listed in the portfolio summary, Brown & Brown (BRO) and Cardinal Health (CAH) appear to be candidates for replacement. Patterson Companies (PDCO) also is a possible candidate for replacement.

Report for February 2006

For the first two months of 2006, the Moose Pond Investors portfolio increased in value by 3.1%. In comparison, the S&P 500 index increased 2.6% for the same period.

The best performing stocks were Investors Financial, IFIN (+22.5%), Jack Henry & Associates, JKHY (+15.3%), and Occidental Petroleum, OXY (+15.1%). The worst performing stock was Intel, INTC (-17.5%).

A performance report for 2006 can be downloaded here.